Britain, November 13, 2015.- We suffer the greatest economic recession of the last hundred years. Each country has faced this economic cycle differently. I have carefully read the diagnosis published in The Guardian. And I have here because it provides data, charts and conclusions that serve for debate and reinforce strategies for the future. The thesis of this English newspaper, one of the most influential is that Britain, has faced this economic downturn better. I invite you to read their arguments:

Blanchflower is absolutely right when he says that it has taken the economy longer to recover from the most recent downturn than it did from any of the other major recessions of the 20th century: the one that came shortly after the end of the first world war, the Great Depression, the stagflation of the mid-1970s, the manufacturing wipe out of the early 1980s, and the housing boom-bust of the early 1990s. This is true even after the latest upward revisions to growth in 2011, 2012 and 2013. Joe Grice, chief economist at the Office for National Statistics, said: “While the profile of the recovery has changed – a weaker initial recovery than previously thought followed by stronger growth between 2011 and 2013 – the overall length and depth of the economic downturn remains very similar to previous estimates. It remains the sharpest downturn and slowest recovery on récord.” Evidence on the state of the economy is scantier for the 18th and 19th century, but a research paper by the Bank of England, shows that economic cycles were relatively short in the 18th century and that the 19th century saw stronger growth with less volatility. Wars tend to cause a lot of economic damage, but in peacetime there has been nothing to compare with the sluggishness of the recovery from the 2008-09 recession.

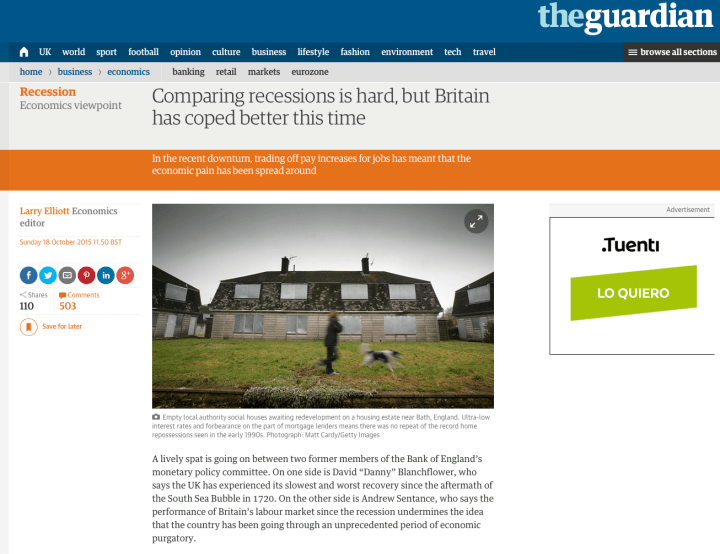

The UK’s performance is even weaker once a rising population is taken into account. The TUC has looked at trends in GDP per head – a more useful measure – and shown that the recovery since the trough of the recession in 2009 has been comfortably weaker than in any similar period since 1842. This chimes with the South Sea Bubble thesis, given the short, sharp nature of 18th Century downturns. But there is a corollary to the squeeze on per capita incomes, and that is the much better-than-expected record for unemployment. Given the severity of the recession in 2008-09, there were forecasts, including by Blanchflower, that unemployment could rise to 5 million. Blanchflower has taken a lot of stick for this prediction, but it was a reasonable judgement in the light of the increases in joblessness suffered in the early 1980s and early 1990s, when the peak to trough drops in output were smaller and unemployment breached the three million level on both occasions. As it turned out, unemployment peaked at just over 8% following the most recent recession compared to over 10% in the early 1990s and 12% in the mid-1980s. The reason was that there was a period of severe pay restraint that held down overall pay bills and so put employers under less pressure to shed staff. In effect, the UK adopted an incomes policy. In the public sector the incomes policy was statutory, with the government imposing below-inflation settlements. In the private sector, it has been voluntary to the extent that when confronted with the choice, workers have decided that they would rather lose a small proportion of their income through a pay cut rather than lose all of it through redundancy.

Britain’s response to the crisis contrasts with France, where both wage growth and unemployment has been higher. French unemployment currently stands at 10.4% – more than double the UK’s joblessness rate. That does not alter the fact that Britain’s economic performance since the financial crisis began in 2007 has been poor. What looked like a promising recovery in late 2009 and early 2010 was snuffed out by policy error (over-aggressive spending cuts and tax increases) and the crisis in the eurozone. Nothing should detract from the fact that this has been an extremely painful period, especially for those who have lost their jobs or been pushed below the breadline. A good recession is an oxymoron.

But trading off pay increases for jobs has meant that the pain has been spread around rather than concentrated in a small segment of the population. It is well established, partly from Blanchflower’s own important work in this area, that unemployment – and especially youth unemployment – has a high social cost, in terms of broken marriages, increased incidence of depression and self harm, ill health and suicide rates. A one percentage point increase in the jobless rate is five times as costly in terms of wellbeing as a one point rise in inflación. That suggests that Britain coped with this recession better than it has with other recessions in the recent past. Ultra-low interest rates and forbearance on the part of mortgage lenders meant there was no repeat of the record home repossessions seen in the early 1990s. Wage cuts limited the increase in unemployment while tax credits have – until now at least – topped up those on low and middle incoes. Clearly, it would have been better had there not been a recession in 2008-09. If George Osborne could have his time again, it is possible that the chancellor would have delayed raising VAT and eased up on his public infrastructure cuts in 2010. But what happened, happened. For sure, this has been the slowest recovery in living memory. The economy has not snapped back in the way it did, for example, when exit from the Exchange Rate Mechanism on Black Wednesday in September 1992 allowed the Major government to slash interest rates. The human cost of the recession and its aftermath was high, but not as high as it would otherwise have been. And, not as high as it was during the period that would win the unwelcome accolade for the most painful episode in Britain’s recent economic history: the early 1980s.

You must be logged in to post a comment.